Stripe is a popular payment platform for SaaS, e-commerce, and marketplace businesses, especially when they need card payments, subscriptions, and seller onboarding. However, many companies start looking for Stripe alternatives when they need lower fees, broader payment method coverage, faster settlement, crypto payments, or better support for specific regions and business models.

Stripe can also be limiting for businesses that work with high-risk industries, need stablecoin settlement, rely on local payment methods, or want more flexibility around payouts and cross-border transactions.

In this guide, we compare the best Stripe alternatives for 2026 based on fees, payment methods, settlement speed, features, and business fit, so you can choose the right provider for your payment stack.

Here are the best Stripe alternatives:

- Square

- PayPal

- NOWPayments

- Stax

- Helcim

- PaymentCloud

- Payanywhere

- Authorize.net

| Alternative | Fee | Speed | Methods | Best for |

| NOWPayments | from 0.3%; 0% for payouts | <1 min payments; <1 sec email payouts | Stablecoins, crypto, payouts, fiat | Crypto payments |

| Square | 2.6% + 10¢; 2.9% + 30¢ | Next day | Cards, wallets, ACH | SMB payments |

| PayPal | 2.9% + fixed fee | 1–3 days | PayPal, cards, banks | Ecommerce trust |

| Stax | $99/mo + interchange | Next day | Cards, wallets, ACH | High-volume sales |

| Helcim | Interchange + markup | 1–2 days | Cards, wallets, ACH | Transparent pricing |

| PaymentCloud | Custom | 1–3 days | Cards, ACH, high-risk | High-risk merchants |

| Payanywhere | 2.69%; 3.49% + 19¢ | Next day | Cards, wallets | Mobile SMBs |

| Authorize.net | 2.9% + 30¢ + $25/mo | 1–3 days | Cards, ACH, wallets | Gateway billing |

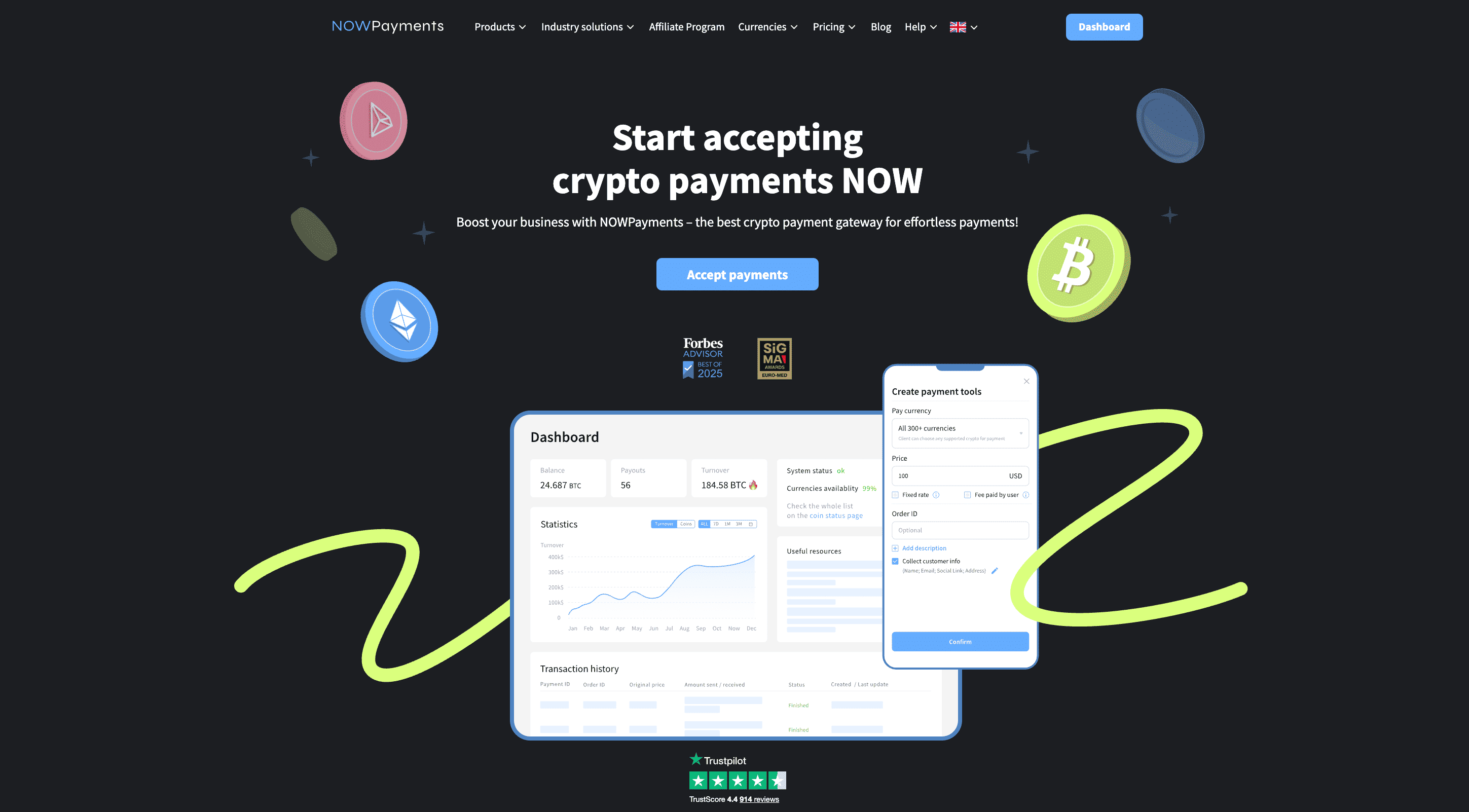

NOWPayments

Best for: enterprises and high-volume businesses that want to accept cryptocurrency and reach global customers without depending only on card rails.

NOWPayments is one of the best alternatives to Stripe for businesses that need a crypto business ecosystem rather than a simple payment gateway. It combines stablecoin payments, mass payouts, conversions, and wallet infrastructure under one platform, with support for USDT and USDC across multiple chains. The service fee ranges from 0.3% to 1%, with custom enterprise rates available on request.

Transaction Fee. NOWPayments uses a competitive service-fee model that ranges from 0.3% to 1% depending on volume, verification level, and currency setup, with custom enterprise pricing available on request. Network fees are paid to the blockchain, not to NOWPayments. Fiat conversions and off-ramp payouts go through partner providers and carry separate fees. The exact rate depends on whether the merchant receives the same asset the customer paid with or uses auto-conversion.

| Transaction type | Fee |

| Single-currency stablecoin | From 0.3% |

| Multi-currency / auto-conversion | From 1% |

| Enterprise / high volume | Custom quote |

Settlement Speed. NOWPayments reports that 99% of crypto payments complete in under one minute once the required blockchain confirmations are reached. Payouts to crypto wallets or custody accounts are typically near-instant. The ecosystem email payout solution can deliver funds in under one second because it uses internal off-chain transfers. Fiat withdrawals depend on partner providers and region.

| Settlement option | Speed |

| Crypto confirmation | <1 min for 99% |

| Wallet / custody payout | Near-instant |

| ChangeNOW Pro Payouts | <1 sec |

| Fiat withdrawal | Depends on partner |

Supported Payment Methods. NOWPayments focuses on stablecoin-first settlement, supporting USDT and USDC across chains such as Ethereum, Tron, BSC, and Polygon. It also supports Bitcoin, Ethereum, and other cryptocurrencies for businesses that want broader coverage. Fiat on- and off-ramp options are available through partner providers in supported regions. The platform is designed for treasury workflows, conversions, cross-border payouts, and mass distributions rather than speculative altcoin acceptance.

| Category | Methods |

| Stablecoins | 30+, incl. USDT, USDC, multi-chain |

| Crypto | BTC, ETH, major coins |

| Fiat | On-/off-ramp partners |

| Payouts | Wallet, custody, email |

Why choose NOWPayments over Stripe:

NOWPayments is a better fit than Stripe for businesses that want to accept stablecoins globally, avoid card chargebacks, and operate outside traditional banking rails. Its mass payout infrastructure and email-based payouts reduce wallet friction for recipients. The ecosystem approach covers payments, payouts, conversions, and custody-style wallets. Merchants still need a card processor for customers who do not use crypto.

Check out NOWPayments’ pricing.

Square

Best for: small retailers, restaurants, and service businesses that need POS and online checkout in one place.

Square is one of the most recognizable Stripe alternatives for small businesses that need both in-person POS and online checkout in a single account. Its US pricing is 2.6% + 10¢ for in-person transactions and 2.9% + 30¢ for online transactions, with no monthly software fee. The platform includes free POS software, inventory tracking, invoicing, and card reader hardware.

Transaction Fee. Square charges a flat rate per transaction and does not require a monthly fee for its core POS and online store. International and keyed-in transactions carry higher rates. The transparent pricing works well for low-volume sellers but becomes less competitive as volume grows. Merchants should compare the effective rate against interchange-plus providers once monthly volume exceeds $50,000–$100,000.

| Transaction type | Fee |

| In-person | 2.6% + 10¢ |

| Online | 2.9% + 30¢ |

| Keyed-in | 3.5% + 15¢ |

Settlement Speed. Authorizations are typically instant across all channels. Standard payouts arrive the next business day. Square also offers instant transfers to a linked debit card for a fee, usually within minutes. Merchants can also schedule same-day transfers depending on eligibility.

| Settlement option | Speed |

| Standard | Next business day |

| Instant transfer | Same day, fee applies |

Supported Payment Methods. Square accepts all major card brands and contactless wallets in person and online. ACH payments and Cash App Pay are available in select markets. The platform supports invoicing, payment links, and QR code payments. In-person sales require Square card readers or terminals.

| Category | Methods |

| Cards | Visa, Mastercard, Amex, Discover |

| Wallets | Apple Pay, Google Pay, Cash App Pay |

| Other | ACH, select markets |

Why choose it over Stripe:

Square is faster to deploy for brick-and-mortar stores because it includes free POS software and native hardware. Stripe offers more developer tools and international coverage, but Square bundles the essentials out of the box. High-volume sellers may eventually save money with interchange-plus providers. For small hybrid businesses, Square’s all-in-one model is often simpler.

Check out Square’s pricing.

PayPal

Best for: online stores that want a widely recognized checkout brand and buyer protection.

PayPal is one of the most familiar alternatives to Stripe for online payments, especially for merchants that value brand recognition and buyer trust. Its standard US online rate is 2.9% plus a fixed fee, with additional cross-border and currency conversion charges. The PayPal wallet is used by hundreds of millions of consumers, which can reduce checkout friction in many markets.

Transaction Fee. PayPal’s standard commercial rate applies to most online transactions, with separate rates for card-funded payments, QR code transactions, and international sales. Cross-border payments add an additional percentage fee, and currency conversion includes a markup. Charities and some nonprofits may qualify for reduced rates. Merchants should model total cost, including fixed fees and cross-border surcharges.

| Transaction type | Fee |

| Standard online | 2.9% + fixed fee |

| Card-funded payment | 1.2% + fixed fee, Advanced |

| International | Domestic rate + cross-border fee |

Settlement Speed. Authorizations are usually instant. Funds reach the merchant’s PayPal balance within minutes. Bank withdrawals typically take one to three business days. Instant transfer to a linked debit card or bank is available for a fee.

| Settlement option | Speed |

| PayPal balance | Minutes |

| Bank withdrawal | 1–3 business days |

| Instant transfer | Minutes, fee applies |

Supported Payment Methods. PayPal supports major credit and debit cards, PayPal wallet balances, bank transfers, and local payment methods in several countries. Venmo is available for US transactions in eligible setups. PayPal Credit and Pay Later options can increase average order value for some merchants.

| Category | Methods |

| Cards | Visa, Mastercard, Amex, Discover |

| Wallets | PayPal, PayPal Credit, Venmo, US |

| Other | Bank transfers, local APMs |

Why choose PayPal over Stripe:

PayPal can improve conversion because many shoppers already have accounts and stored payment methods. Its buyer and seller protection programs add a layer of trust for both parties. The trade-offs are higher effective fees, especially on international transactions, and occasional account holds or limited support during disputes.

Check out PayPal merchant fees

Stax

Best for: US businesses with steady, high transaction volume or recurring revenue models.

Stax is a subscription-based payment processor like Stripe that targets high-volume US merchants with recurring revenue. Instead of adding a percentage markup on every sale, it charges a flat monthly subscription starting at $99 plus interchange and a small per-transaction fee. This model can lower the effective rate for businesses processing tens of thousands of dollars per month or more.

Transaction Fee. Stax passes interchange at cost and adds a subscription fee plus per-transaction charges. The entry subscription is $99 per month for businesses processing up to $150,000 annually; higher tiers are $139 and $199. In-person transactions add 8¢ above interchange, while online or keyed transactions add 15¢. Enterprise merchants can request custom pricing.

| Plan component | Fee |

| Monthly subscription | From $99/mo |

| In-person | Interchange + 8¢ |

| Online/keyed transaction | Interchange + 15¢ |

Settlement Speed. Authorizations are instant. Standard funding is next business day. Same-day funding is available for an additional fee in eligible cases. Settlement timing depends on the linked bank account and transaction time.

| Settlement option | Speed |

| Standard | Next business day |

| Same-day | Available, fee applies |

Supported Payment Methods. Stax supports card payments, digital wallets, and ACH through its platform. It also offers invoicing, payment links, text-to-pay, and recurring billing. The platform integrates with many POS systems and business apps via prebuilt connectors and Zapier.

| Category | Methods |

| Cards | Visa, Mastercard, Amex, Discover |

| Wallets | Apple Pay, Google Pay |

| Other | ACH |

Why choose Stax over Stripe:

Stax can lower the effective rate for high-volume merchants because it does not add a percentage markup on top of interchange. The subscription model also makes costs predictable. The trade-off is the monthly fee, which is hard to justify for smaller businesses. Merchants focused purely on online international sales may find Stripe’s global coverage stronger.

Check out Stax’s pricing

Helcim

Best for: established SMBs, B2B sellers, and subscription businesses in the US and Canada.

Helcim is a transparent, cheaper alternative to Stripe for US and Canadian businesses that process enough volume to benefit from interchange-plus pricing. It charges no monthly platform fee and automatically lowers rates as monthly processing volume grows. The published starting rates are interchange plus 0.40% and 8¢ for in-person transactions and interchange plus 0.50% and 25¢ for online transactions.

Transaction Fee. Helcim publishes interchange-plus rates with no monthly platform fee. Rates drop automatically at higher monthly volumes. ACH transfers carry a separate fee. There are no setup fees, PCI fees, or cancellation fees.

| Transaction type | Fee |

| In-person | Interchange + 0.40% + 8¢ |

| Online | Interchange + 0.50% + 25¢ |

| ACH | 0.5% + 25¢, capped |

Settlement Speed. Authorizations are instant. Standard settlement takes one to two business days. Helcim does not advertise same-day funding, so businesses that need daily cash flow should confirm timing before signing.

| Settlement option | Speed |

| Standard | 1–2 business days |

Supported Payment Methods. Helcim supports major card brands, digital wallets, and ACH transfers. It also provides POS software, virtual terminal, invoicing, and recurring billing. The platform is available in USD and CAD.

| Category | Methods |

| Cards | Visa, Mastercard, Amex, Discover |

| Wallets | Apple Pay, Google Pay |

| Other | ACH |

Why choose Helcim over Stripe:

Helcim’s transparent pricing and automatic volume discounts can reduce costs for merchants processing $10,000 or more per month. There are no monthly fees or long-term contracts. The main limitations are geographic coverage and lack of high-risk support. International sellers should consider a processor with broader multi-currency support.

Check out Helcim’s pricing

PaymentCloud

Best for: businesses in high-risk industries that struggle to get approved by mainstream processors.

PaymentCloud is one of the few companies like Stripe that focuses on hard-to-place and high-risk merchant accounts. It matches businesses with partner acquiring banks rather than acting as a direct processor, which allows it to support industries that mainstream providers decline. Pricing is quote-only and depends on risk profile, industry, and volume.

Transaction Fee. PaymentCloud does not publish standard rates; fees are set during underwriting. Reported ranges for high-risk merchants typically start around 2.7%–4.3% plus a per-transaction fee, though exact pricing varies. Many setups use a partner gateway such as Authorize.net, which may add a monthly gateway fee. Merchants should request a full fee schedule before signing.

| Pricing model | Fee |

| Transaction fee | Custom quote |

| Monthly gateway fee | Varies by partner |

| High-risk premium | Above standard rates |

Settlement Speed. Approval and settlement timing depend on the matched acquiring bank. Many merchants receive next-day to three-day settlement once approved. High-risk accounts may be subject to rolling reserves or delayed funding. Merchants should confirm reserve terms during underwriting.

| Settlement option | Speed |

| Standard | 1–3 business days |

| Rolling reserve | Possible, risk-based |

Supported Payment Methods. PaymentCloud supports card and ACH processing through partner gateways. Crypto acceptance is available via partners. The platform connects to major shopping carts such as Shopify, WooCommerce, and Magento.

| Category | Methods |

| Cards | Major credit/debit cards |

| Other | ACH, e-check, crypto via partners |

Why choose PaymentCloud over Stripe:

PaymentCloud can approve businesses that Stripe declines due to industry or risk profile. It provides dedicated account managers and chargeback mitigation tools. Merchants should expect higher fees and possible reserves compared to mainstream processors. It is not the right choice for low-risk or low-volume businesses.

Check out PaymentCloud

Payanywhere

Best for: US-based mobile vendors, service providers, and small retailers that mainly take in-person payments

Payanywhere is a mobile-first Stripe payment alternative for US-based small businesses and contractors. It offers card readers, a mobile POS app, and next-day funding. Its in-person rate is 2.69% for tapped, dipped, or swiped transactions, while keyed, online, and invoiced transactions cost 3.49% plus 19¢.

Transaction Fee. Payanywhere uses flat-rate pricing with no monthly software fee for basic mobile processing. Online, keyed, and invoiced transactions cost more than swiped or tapped payments. Merchants should review the full agreement for additional fees such as chargebacks, NSF, or equipment-related costs.

| Transaction type | Fee |

| Tapped, dipped, swiped | 2.69% |

| Keyed, online, invoiced | 3.49% + 19¢ |

Settlement Speed. Authorizations are instant. Standard funding is next business day. Same-day funding is available for an additional fee. Settlement timing depends on the merchant’s bank and funding schedule.

| Settlement option | Speed |

| Standard | Next business day |

| Same-day funding | Available, fee applies |

Supported Payment Methods. Payanywhere supports major credit and debit cards plus contactless wallets through its mobile readers and terminals. It also offers a virtual terminal and invoicing. In-person payments require Payanywhere hardware.

| Category | Methods |

| Cards | Visa, Mastercard, Amex, Discover |

| Wallets | Apple Pay, Google Pay, Samsung Pay |

Why choose Payanywhere over Stripe:

Payanywhere is practical for field-based sellers who need a mobile POS without monthly software fees. Its in-person rate is competitive for small tickets. Online sellers or businesses needing advanced reporting may outgrow it quickly. Merchants should also review customer feedback on fee transparency before signing.

Check out Payanywhere pricing

Authorize.net

Best for: businesses that need a standalone gateway with recurring billing and fraud tools.

Authorize.net is one of the longest-running Stripe competitors, offering a payment gateway with optional merchant account bundles. It is owned by Visa and is widely used by established US and Canadian businesses. The all-in-one plan costs $25 per month plus 2.9% and 30¢ per transaction.

Transaction Fee. Authorize.net offers an all-in-one plan or a gateway-only plan. The all-in-one plan includes a merchant account and gateway for $25 per month plus 2.9% and 30¢ per transaction. The gateway-only plan costs $25 per month plus 10¢ per transaction and a daily batch fee, but requires a separate merchant account.

| Plan | Fee |

| All-in-one | 2.9% + 30¢ + $25/mo |

| Gateway only | $25/mo + 10¢/transaction |

Settlement Speed. Authorizations are instant. Settlement timing depends on the linked merchant account, usually one to three business days. Same-day funding may be available through the merchant account provider. Merchants should confirm timing with their bank or processor.

| Settlement option | Speed |

| Standard | 1–3 business days |

Supported Payment Methods. Authorize.net supports major credit and debit cards, digital wallets, and ACH/e-checks. It includes recurring billing, customer information management, and advanced fraud detection. The platform integrates with many ecommerce carts and business systems.

| Category | Methods |

| Cards | Visa, Mastercard, Amex, Discover |

| Wallets | Apple Pay, Google Pay, PayPal |

| Other | ACH/e-check |

Why choose Authorize.net over Stripe:

Authorize.net lets merchants keep their existing merchant account and banking relationship while adding a reliable gateway. Its recurring billing and fraud tools are mature. The monthly gateway fee and regional limits make it less attractive for new or international businesses. Merchants processing over $500,000 per year may qualify for custom pricing.

Check out Authorize.net pricing

How to Choose the Best Stripe Alternative

Before switching from Stripe, compare providers based on the criteria that matter for your business model:

- Fees: flat-rate, interchange-plus, or subscription-based pricing.

- Speed: authorization time and settlement speed.

- Mass payouts: important for marketplaces, affiliates, and contractors.

- Supported countries: where you sell and where you can settle.

- Payment methods: cards, wallets, bank transfers, and crypto.

- Crypto support: only some providers, like NOWPayments, support digital assets natively.

- Settlement speed: next-day settlement vs. 1–3 business days.

- Integrations: e-commerce platforms, CRMs, and accounting tools.

- Risk policy: approval speed, reserves, and accepted industries.

- Business model fit: retail, SaaS, subscriptions, high-risk, or global e-commerce.

Conclusion

Stripe remains a strong platform, but it is not the only choice. The best Stripe alternatives in 2026 range from card processors like Square and Helcim to specialized options like PaymentCloud and NOWPayments.

If you are looking for a Stripe alternative that supports crypto payments, explore NOWPayments as a Stripe alternative.

FAQ

What is the best Stripe alternative?

The best Stripe alternative depends on your business. Square suits in-person sellers, PayPal works for e-commerce trust, Stax fits high-volume subscriptions, and NOWPayments is a strong option for crypto payments.

Which Stripe alternative is best for crypto payments?

NOWPayments as a Stripe alternative is built for crypto. It supports 30+ stablecoins, mass payouts, and fiat conversion, though it is not a full replacement for card acquiring.

Is NOWPayments a good Stripe alternative?

NOWPayments is a good crypto-friendly Stripe alternative for businesses that want to accept digital assets globally and reduce reliance on card rails. It is less suited if your customers primarily pay by card.

What should I check before switching from Stripe?

Compare total fees, settlement speed, supported countries, chargeback policies, and integration effort. Also confirm whether the provider accepts your industry and risk profile.

Are crypto payment gateways a good alternative to Stripe?

Crypto gateways can be a useful alternative to Stripe for borderless payments, lower crypto service fees, and no chargebacks. They work best as part of a multi-payment strategy rather than a full replacement.